February 2026 Market Update

February 2026 Market Update  January 1, 2026

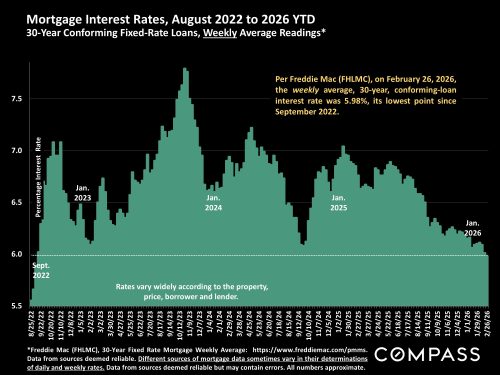

January 1, 2026  Market Update, November 1, 2025

Market Update, November 1, 2025  Just Listed in Old Palo Alto

Just Listed in Old Palo Alto  Just Listed in Portola Valley

Just Listed in Portola Valley State Farm and Allstate have announced they will no longer sell new home insurance policies in California because of wildfire risks and an increase in construction costs. Here are some facts:

- State Farm and Allstate are not leaving the California Insurance Market: State Farm and Allstate will continue to service and renew policies of existing clients in the state and will continue to offer new auto insurance policies. However, they will not be issuing any new property insurance policies for the time being in California.

- What are the implications of the decision for prospective homebuyers? In certain high-risk areas of the state, there are very few insurance companies willing to write new policies. In some higher risk areas, State Farm was the last private insurance company writing policies. In those areas, unless the Insurance Commissioner is successful in its effort to get more private insurers to write policies in such areas, the generally more-costly California FAIR plan may end up being the only property insurance available.

- Why did State Farm and Allstate stop issuing new policies? State Farm stated that it made the decision “due to historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market.” Allstate said the company “paused” its offerings “so they can continue to protect current customers.” State Farm and Allstate’s decision is not necessarily an indication of what other companies will do.

- Will more companies follow State Farm and Allstate’s move? There are still a wide range of companies writing policies in California. However, those willing to write new policies in higher risk areas in particular are declining and as stated above, with the departure of State Farm and Allstate, those in more high-risk areas may have no option than the FAIR plan.

- What are the main problems for the insurance market in California? The California market is heavily regulated and has various strict requirements for rate increases, which were put into place by Proposition 103 in 1988. However, there are two areas where possible changes could result in a better climate for insurance without requiring major changes to consumer-friendly rate increase requirements. Those include allowing insurance companies to have rates that better reflect their reinsurance costs and allowing insurance companies to utilize forward looking risk models. Current law only allows companies to look back when setting rates. However, given the issues with climate change, many insurance companies argue that looking backward does not allow companies to adequately capture risk.

- Where can I direct my clients for information if they are looking for homeowners insurance? The California Dept. of Insurance provides several information guides, tips and tools to help them understand home/residential insurance so that they can make the best decision for their situation. They can also call the California Dept. of Insurance Consumer Hotline for assistance.

- What is C.A.R. doing? C.A.R. has been in discussions with both the Insurance Industry representatives and the Department of Insurance on State Farm and Allstate’s move and other homeowner insurance issues. The Insurance Industry and the Department of Insurance have also been looking at and discussing ways to address the state’s insurance challenges. The issue is large and complicated. We have cautious hope that these moves may create some greater urgency on how to address this insurance situation.

Source: C.A.R.