February 2026 Market Update

February 2026 Market Update  January 1, 2026

January 1, 2026  Market Update, November 1, 2025

Market Update, November 1, 2025  Just Listed in Old Palo Alto

Just Listed in Old Palo Alto  Just Listed in Portola Valley

Just Listed in Portola Valley It’s hard to put a positive spin on recent economic and political realities. It’s good news that Powell has signaled that the Fed will hold off on a monthly increase in the Fed rate, but doesn’t change the basic situation of steadily increasing interest rates.

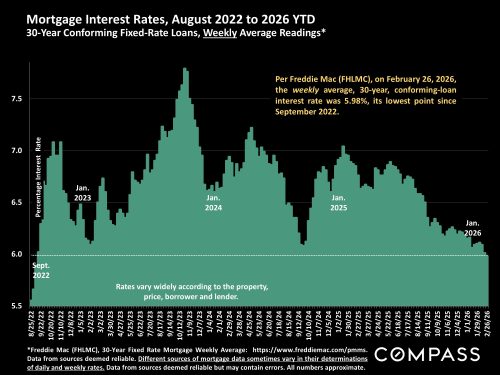

Here are 3 angles on interest rates over varying periods of time: average daily, average weekly, and jumbo loan rates (all of which use different methodologies in their calculations):

Stock markets through yesterday. Still well up for the year, but well down from the YTD mid-summer high. As of this morning, they are falling again (but this can change very quickly):

According to NAR, The national percentage of all-cash buyers in September was at its highest point in 8+ years. An increased percentage of total sales does not necessarily mean an increase in the actual number of all-cash buyers. But as a share of the market, all-cash buyers are participating more actively than those requiring loans.

NAR released September sales data yesterday. Below is the chart on national single family home prices since 1990. Though many Bay Area markets have seen strong, sometimes very strong, rebounds in median sales prices in 2023, generally speaking, the overall national market has rebounded closer to 2022 peak house prices.