February 2026 Market Update

February 2026 Market Update  January 1, 2026

January 1, 2026  Market Update, November 1, 2025

Market Update, November 1, 2025  Just Listed in Old Palo Alto

Just Listed in Old Palo Alto  Just Listed in Portola Valley

Just Listed in Portola Valley The inflation reading for October, released yesterday, declined – from 3.7% to 3.2% for the overall index, and from 4.1% to 4% for the “core” index – fueling a continuation of the very dramatic stock market rebound that began on November 1st with the Fed’s pause on rate hikes.

Soaring stock markets: The percentages below reference changes in the stock market indices since the year began, but one can see the tremendous jump that has occurred in the last 2 weeks.

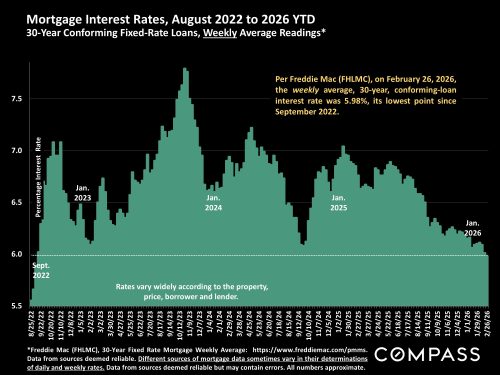

The daily average interest rate – illustrated below – is roughly where it was after the big decline in early November (after the Fed announcement of a continued pause in Fed benchmark rate increases) – substantially down from October highs. The 11/15/23 reading was 7.45%. The new weekly average reading from Freddie Mac comes out tomorrow, but based on interest rate changes over the last week, it seems likely to stay relatively close to last week’s reading (7.5%).

Freddie Mac’s weekly average reading will be updated tomorrow, 11/16/23 @ https://www.freddiemac.com/pmms

Jumbo loan rate chart: As of yesterday’s reading, running at about 7.6%.

4 charts from an updated Bay Area market survey. (PDF & JPGs are in this folder). The survey includes several comparisons of our current market with the pre-pandemic market in 2019. I’ve included Sacramento County in the first 3 charts below.

Median house sales price appreciation since autumn 2019:

Comparative median $/sq.ft. house values:

Percentage home sales declines – in # of residential sales reported to MLS – since autumn 2019:

In this YTD comparison with 2019 luxury home sales, the “luxury home” category is defined as $5 million+ in the 4 most expensive counties (SF, Marin, Santa Clara, San Mateo), and as $3 million+ in the other counties.

The national unemployment rate ticked up slightly in October – which financial markets liked since it indicated some cooling in the economy, which presumably influenced the Fed in their decision not to raise the benchmark rate – but remains close to historic lows.

October unemployment data for the Bay Area has not been released yet, but through September, the general picture is similar: Close to historic lows.